Quarterly Market Review

Martin Boulianne - Apr 08, 2026

The first quarter of 2026 was marked by increased market volatility as investors navigated slower economic growth, lingering inflation, and uncertainty around interest rates. These conditions weighed on risk‑oriented assets and led to declines across

April 3,2026

Period Ended March 31, 2026

Prepared by:

Martin Boulianne, CPA, FCSI

Anthony Zicha, BSc., CIM, FCSI

Q1 2026 Market Update & Portfolio Commentary

A volatile start to the year

The first quarter of 2026 was marked by increased market volatility as investors navigated slower economic growth, lingering inflation, and uncertainty around interest rates. These conditions weighed on risk‑oriented assets and led to declines across many equity markets.

On the portfolio side, our Special Situations and TSX core holdings benefited from strength in Alamos Gold Inc., Lundin Gold Inc., MDA Space Ltd., and Telesat Corp., with additional support from energy exposure through Methanex Corporation.

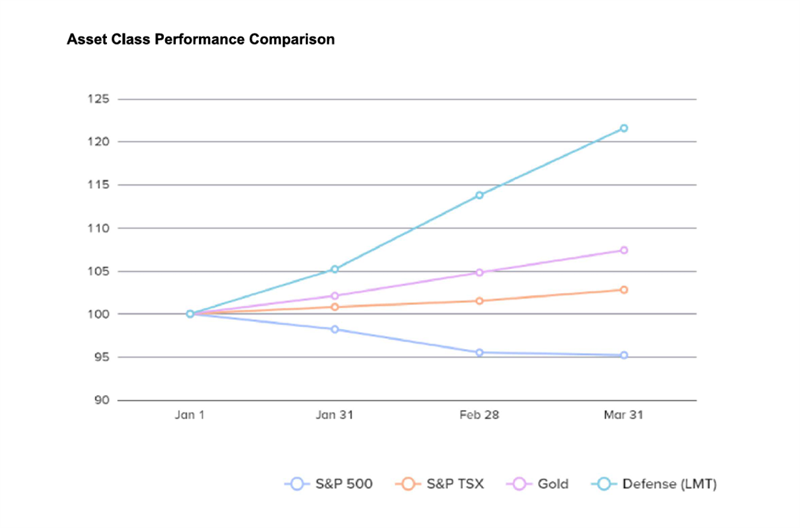

While periods like this can be uncomfortable, they are a normal part of investing. Heightened geopolitical tensions contributed to short-term market swings, with U.S. equities declining 4.81% and Canadian markets rising 2.77%, supported by energy strength.

Exposure to defensive areas such as gold, defense, and space technology helped provide stability and cushion portfolios during the quarter.

Source:LSEG

The War Premium: Understanding Market Volatility

Iran Conflict Timeline and Impact

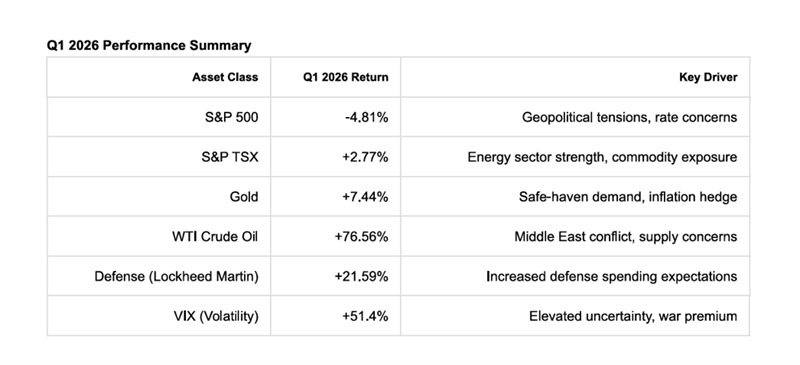

Early March 2026 saw U.S. and Israeli air strikes on Iran, marking a significant escalation in Middle East tensions. Markets responded with textbook risk-off behavior:

- VIX volatility index surged 51% (from 16.53 to 25.02)

- WTI crude oil rose 76.56% to breach $100/barrel

- Gold advanced 7.44%

- Defense stocks rallied (Lockheed Martin +21.59%)

![]()

Source: LSEG

Historical Perspective: Markets and War

Historical data shows that geopolitical shocks typically create short-term volatility but have not consistently derailed long-term bull markets. Initial selling pressure has historically given way to reassessment of economic fundamentals. Markets recovered 6-12 months after major conflict outbreaks in cases where:

- Conflicts remained regionally contained

- Global supply chains adapted

- Central banks maintained accommodative stances

- Corporate earnings remained resilient

How markets performed

Canadian and U.S. equity markets were volatile during the quarter, with economically sensitive areas most affected. Smaller and mid‑sized companies saw steeper drawdowns than large, established businesses, reflecting investor caution and a preference for balance‑sheet strength. At the same time, cash and short‑term instruments provided stability and helped reduce overall portfolio volatility, reinforcing their role as an important buffer during uncertain markets.

Source:LSEG

Industrial sector performance: Canada and the U.S.

Industrial companies in both Canada and the United States experienced a difficult quarter, though for slightly different reasons.

In Canada, industrial products and services were impacted by:

- Slower domestic economic activity

- Reduced capital spending

- Investor concern around margins and input costs

Despite these short‑term headwinds, many Canadian industrial businesses continue to benefit from solid order backlogs, long‑term infrastructure needs, and strong balance sheets. While prices pulled back during the quarter, the fundamentals of these companies remain intact.

In the United States, industrial stocks also declined as markets reassessed growth expectations. Higher financing costs and cautious corporate spending weighed on sentiment. However, U.S. industrial companies tied to infrastructure, defense, and automation continue to show strong long‑term growth potential, even if near‑term results are uneven.

In both markets, we view the recent weakness as cyclical rather than structural. Well‑run industrial businesses often emerge stronger after periods of economic slowdown.

Portfolio positioning and risk management

Throughout the quarter, portfolios remained deliberately diversified across sectors, geographies, and asset classes. This diversification helped limit drawdowns relative to more concentrated investment approaches.

We continue to focus on:

- High‑quality businesses with strong cash flows

- Reasonable valuations

- Companies capable of navigating slower economic environments

Where appropriate, we selectively added to positions where volatility created attractive long‑term entry points.

Looking Ahead

Market downturns are never comfortable, but they often create the foundation for future gains. History consistently shows that investors who remain patient and disciplined through periods of uncertainty are well positioned to benefit over time.

Looking forward, we remain optimistic. Inflation continues to show signs of stabilizing, interest‑rate expectations are becoming clearer, and economic growth—while moderating—remains intact. Together, these dynamics can support a more constructive investment backdrop in the quarters ahead.

Market Outlook: Key Trends and Scenarios

Near Term (3–6 months)

Geopolitical‑related volatility may begin to moderate as markets adapt to the evolving global environment. While trading conditions could remain uneven in the near term, oil prices are expected to move toward equilibrium and interest‑rate expectations should continue to be firm. Canadian markets may maintain relative strength, supported by their meaningful exposure to commodity‑oriented sectors.

Medium Term (6–12 months)

Historical patterns following conflict‑driven market disruptions suggest that recovery phases often develop as:

- Geopolitical conditions stabilize through containment or de‑escalation

- Oil prices normalize toward historical post‑shock ranges ($70–$85)

- Corporate earnings visibility improves

- Central banks provide clearer guidance on policy direction

Key Risk Factors to Monitor

- Escalation of conflicts beyond their current scope

- Sustained oil prices above $100 and potential impacts on global demand

- Shifts in central‑bank policy or communication

- Corporate earnings reflecting margin pressures

Most importantly, your portfolio remains aligned with your long‑term objectives, risk tolerance, and income needs. Our approach remains focused on building resilient portfolios designed to navigate short‑term volatility while positioning for long‑term growth across full market cycles.

As always, we truly appreciate your continued trust and confidence. If you have any questions about this report or would like to discuss positioning in more detail, please don’t hesitate to reach out.